Description

Computes an exponentially smoothed version of the input Block over a ranking Dimension.

Syntax

SIMPLE_EXPONENTIAL_SMOOTHING(Input Block [, Ranking Dimension [, alpha]})

Arguments

| Argument | Type | Dimensions | Description |

|---|---|---|---|

| Input Block (required) | Number | Any Dimensions | This is the data source which will be smoothed. The Metric must be defined at least on the Ranking Dimension Dimension. |

| Ranking Dimension (optional) | Dimension | Not applicable | This is a Dimension applied to the time series taken in the Input Block. This is optional if it’s a datetime Dimension from the calendar. If this is not the case, then this is mandatory. It’s also mandatory if the Metric is defined on several time Dimensions. |

| alpha (optional) | Number | no Dimension | Data smoothing factor, with a value between 0 and 1. The default value is 0.5 . |

Returns

| Type | Dimensions |

|---|---|

| Number | Dimensions of Input Block |

- Before the first non-blank value of the Input Block, the function returns blank.

- Between the first and the last non-blank value of the Input Block, the function returns the following values:

- for the first non blank value, the function return the same, this is shown in the s0 value in the equation below.

- for other values the function computes a weighted average between the current value and the previous smoothed value.

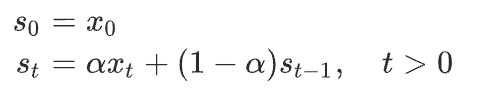

Here is an equivalent with mathematical notations (s being the exponentially smoothed version of the x serie):

- After the last non-blank value of the Input Block, the function returns a constant value equal to the last smoothed value computed.

Blank observations (in the input Block) between the first non-blank value and the last non-blank values are considered as 0.

Examples

| Formula | Description |

|---|---|

SIMPLE_EXPONENTIAL_SMOOTHING(Actuals) | Returned values are explained in the Returns section above. |

SIMPLE_EXPONENTIAL_SMOOTHING(Actuals, Month, 0.2) |

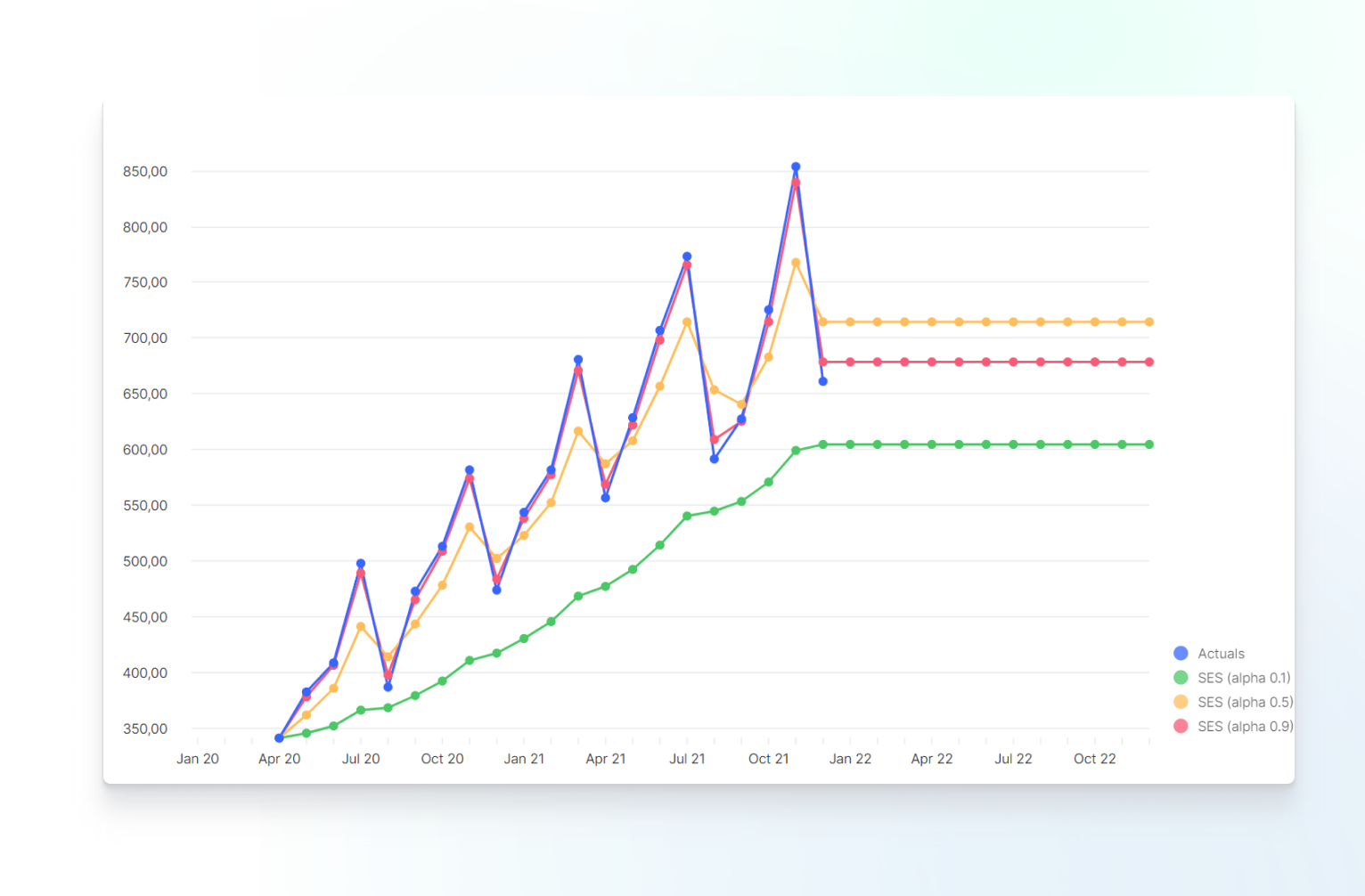

Examples with different values of alpha:

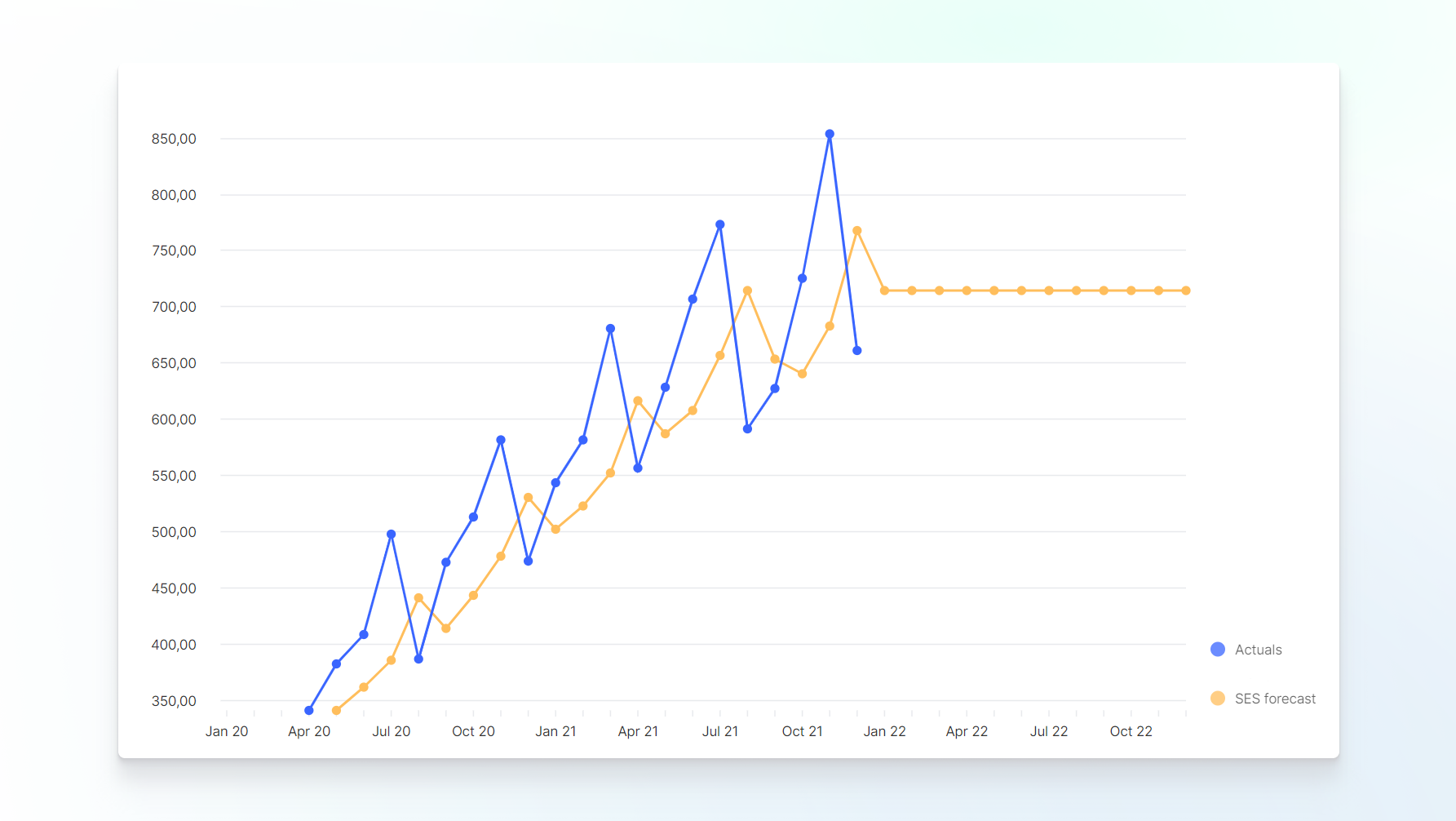

Using Exponential Smoothing as Forecasting Function

A common use case for using the SIMPLE_EXPONENTIAL_SMOOTHING function is to prepare a forecast. It’s a good method when your observation series shows no specific trend and no specific seasonality.

In that case the last smoothed value of the series is a good estimation of the next forecasted value. To do so you just need to offset the result by 1 period with this syntax:

SIMPLE_EXPONENTIAL_SMOOTHING(Observations)[SELECT: Month -1]

See also

Excel: no equivalent

Related articles: None

References: Wikipedia Exponential Smoothing